- The 2024 energy reform establishes the State’s prevalence in electricity generation and commercialization: at least 54% of the energy injected into the grid must belong to the State in one of the forms of participation established by law, while energy generated by private investors can account for up to 46%. This prevalence is calculated annually and enforced through binding planning, which determines the projects and permits to be granted to both State and private initiatives.

- Under the current rules for private energy generation, the State decides where each generation plant is built, what renewable technology it will use (wind and photovoltaic, but not natural gas, which is non-renewable), where it will connect to the National Electric System (which interconnection substation), and its year of commissioning. All of this comes with very tight planning horizons, approvals, and payment deadlines for projects of this scale.

- Private investors, whether national or foreign, must accept the call for projects under these terms, covering planning costs and financial commitments prior to receiving the permit, and must express interest within just five days.

- Pre-permit costs mainly come from connecting to transmission lines within the substation, which is owned by CFE. This is not an industry standard, as typically the substation owner covers interconnection costs. In Mexico, CFE is responsible for the substations that receive new renewable generation projects.

- The private investor’s planning horizon is limited to five business days from the October 17, 2025 call. As a result, they must pay substantial upfront costs and have very little time to decide and notify the National Energy Commission of their interest in participating, until the next call is issued (with an uncertain date).

- Evolution of the Legal Framework

- State Prevalence in the Electricity Sector

- Expected Participation of the Private Sector

- Proposed State Participation

- Analysis of Electricity Demand Integrated into Binding Planning

- Transparency and Best Practices in the Energy Model

- Risks and Advantages of the New Model

- Final Remarks

Context of Renewable Energy in Mexico

The 2024 energy reform establishes the State’s prevalence in electricity generation and commercialization. This means at least 54% of the energy injected into the grid must belong to the State in one of the forms of participation established by law, while energy generated by private investors can contribute up to 46%. This prevalence is calculated annually and enforced through binding planning, which determines the projects and permits for both State and private initiatives.

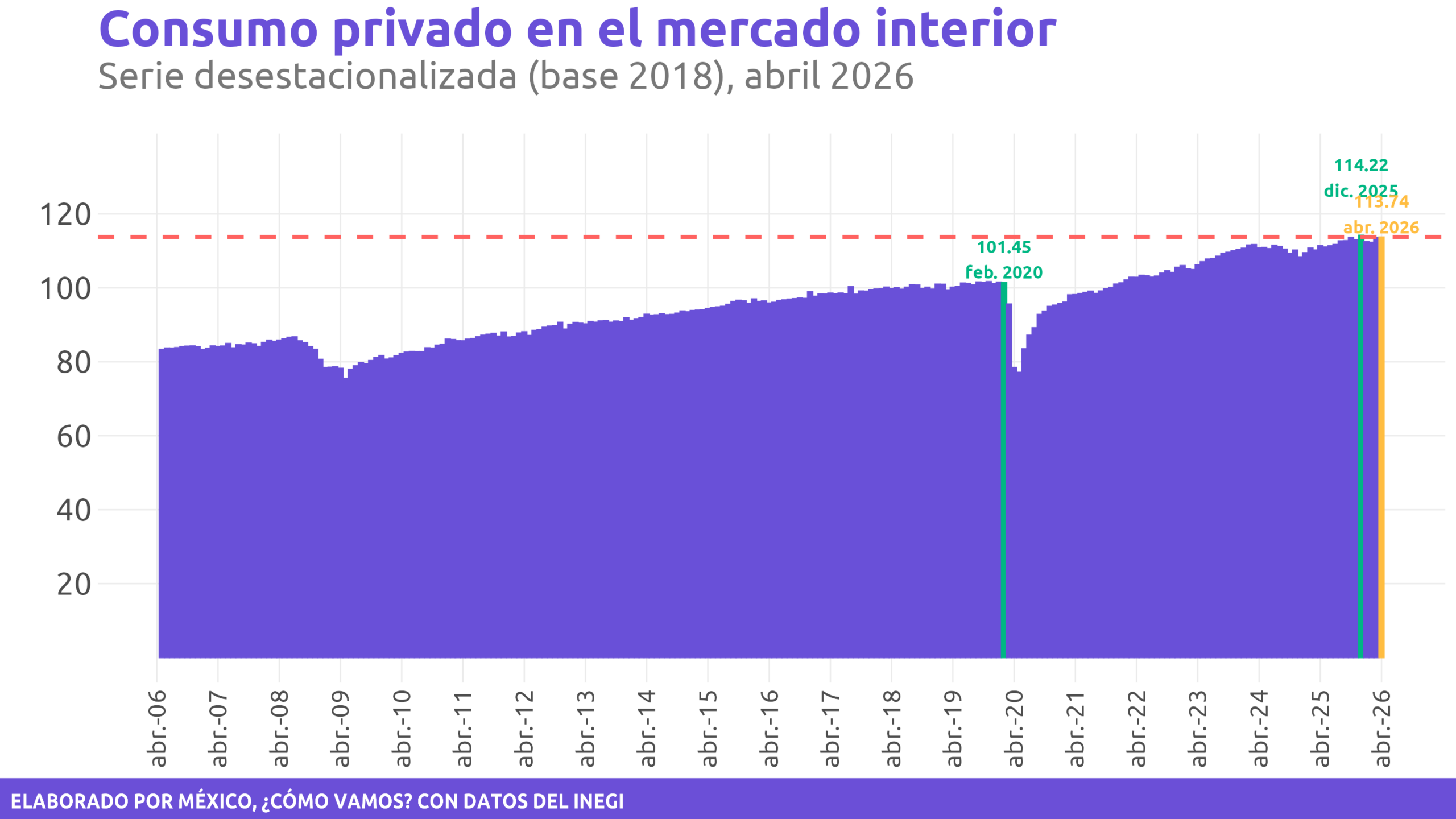

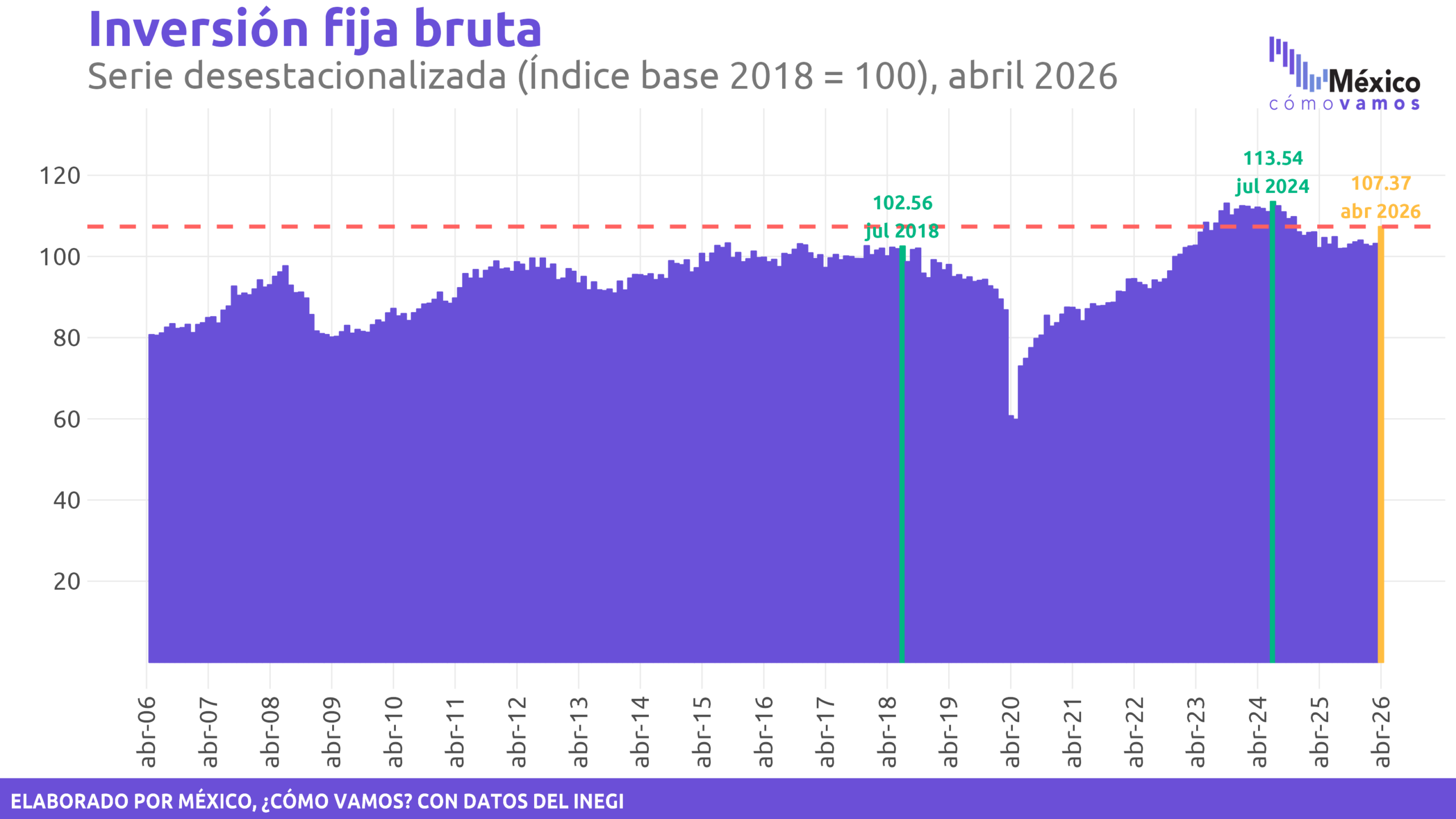

Private investors can participate in mixed projects, long-term contracts, plants that compete with the State, and self-consumption schemes, always within current constitutional limits. Regulatory incentives favor partnerships with the State, as strategic projects receive streamlined permitting and CFE operates as a vertically integrated monopoly not subject to competition regulation. However, to leverage private investment—which represents around 90% of total gross fixed investment in Mexico—clearer regulations are needed to remove doubts about operations, maintenance, and optimal performance of new generation projects.

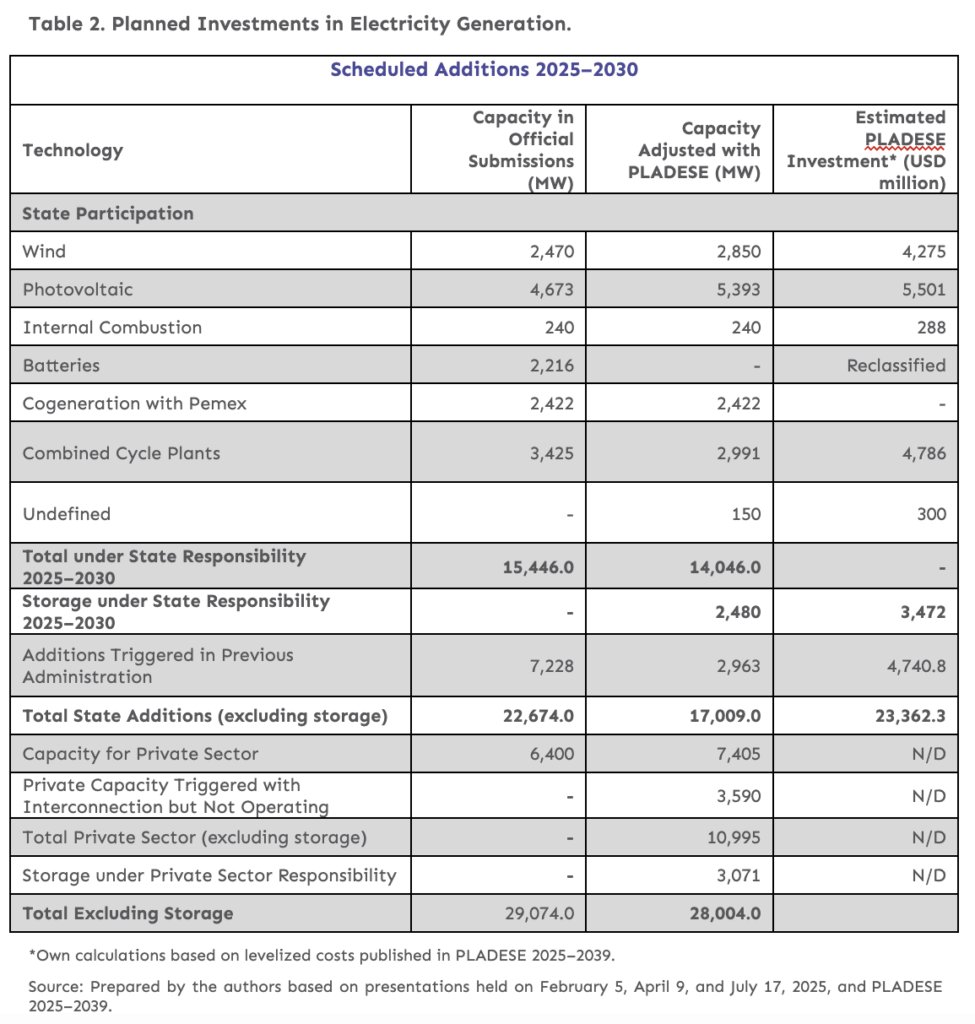

The 2025-2030 Electric Development Plan (PLADESE, by its Spanish abbreviation), published in the Official Federal Gazette on October 17, 2025, aims to double current installed renewable capacity. That is, add 28,004 MW of capacity (excluding storage), about 80% of which is expected to be clean or renewable energy. Total estimated investment in state-participation generation projects is $23,362 billion USD, in addition to significant investments in transmission and distribution. The goal is for private investors to fund the bulk of this plan.

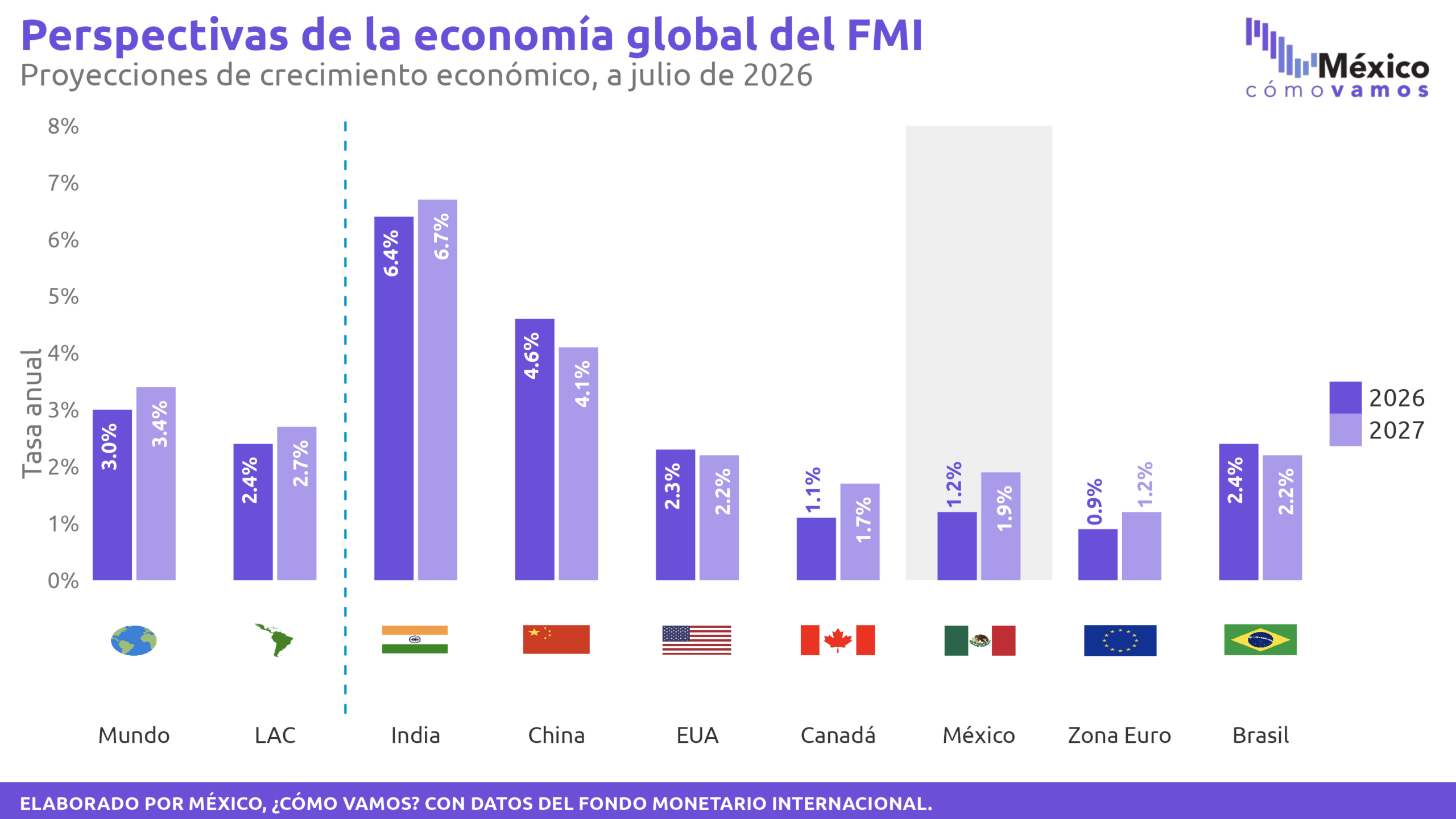

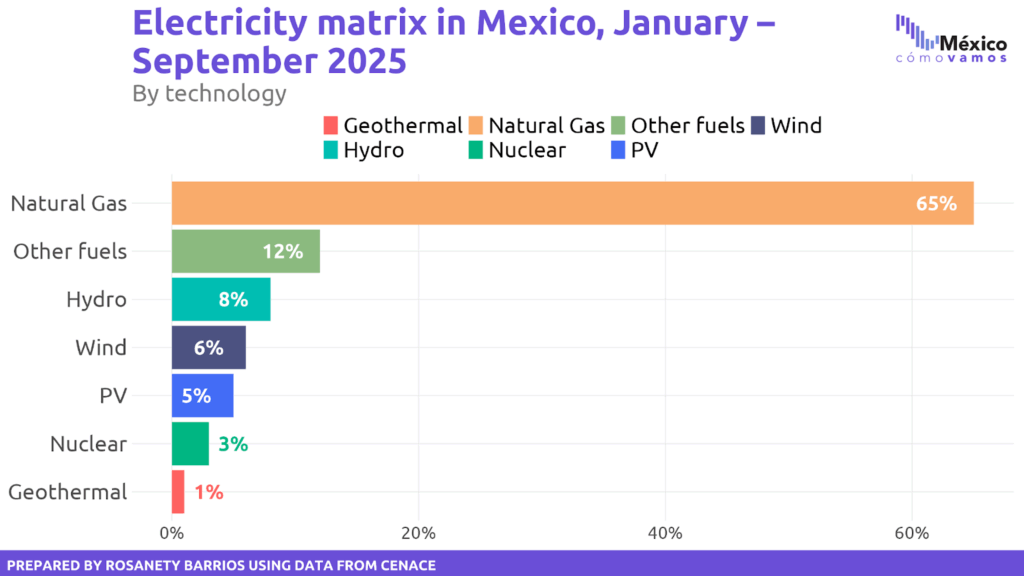

This target aligns with international commitments, aiming for 38% clean generation. Current electricity generation (January–September 2025) relies 77% on fuels and 23% on clean energy.

Annual electricity demand is expected to grow 2.5% between 2024 and 2038, in line with a projected 2.5% economic growth per year. The current model prioritizes tariff stability (adjusted for inflation) over price reduction, and poses challenges for transparency and competition, since project allocation may not be fully open or competitive.The model’s success depends on clear contracts, on how timely and effectively the State manages calls for private participation, on the efficient operation of the plants, and on the State’s ability to deliver the planned electricity supply. There are systemic risks tied to judicial independence and the renegotiation of the USMCA, but there are also advantages thanks to Mexico’s trade relationship with the United States.

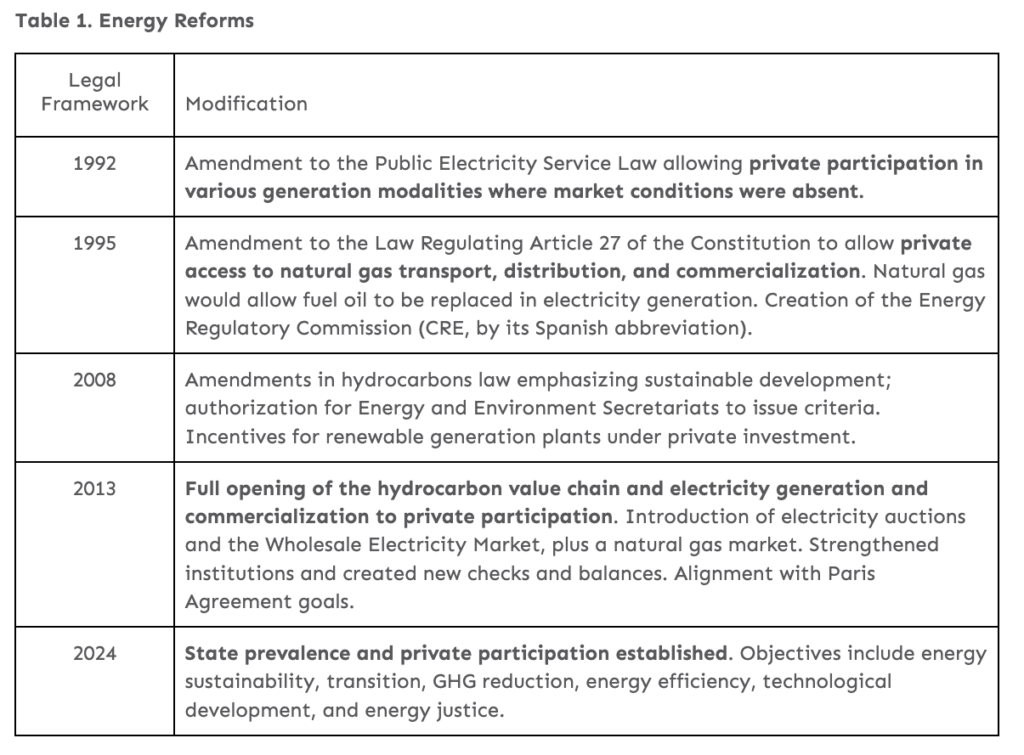

1. Evolution of the Legal Framework

Over the past 30 years, Mexico has undergone five energy reforms. The first three were legal in nature, while the last two required constitutional amendments.

All reforms share common objectives: modernizing the sector, reducing emissions, and institutionalizing market participants—all within a mixed development model established by the Constitution. In fact, in the first four reforms, there was recognition of the high cost of energy in Mexico, which led to goals for reducing prices and tariffs—a goal that disappeared in the 2024 reform and was replaced by a commitment to growth with prices and tariffs adjusted for inflation.

The first three reforms gradually opened the sector to private investment and created markets, requiring alignment of all participants’ interests, including State-owned companies. However, with the 2013 Reform, these companies were forced to compete in some activities with the private sector, a requirement that was eliminated under the concept of prevalence in the 2024 reform.

2. State Prevalence in the Electricity Sector

The October 2024 constitutional amendment on strategic enterprises establishes “the non-prevalence of private entities over State-owned companies” in electricity generation and commercialization.

Analysis of the Electric Industry Law and its regulations shows that State prevalence is the main difference compared to previous legal frameworks. While the Constitution establishes the “non-prevalence” of private investors over the State, the Electric Industry Law, in contrario sensu, develops the concept of State prevalence and defines its scope.

The Electric Sector Law (LESE, by its Spanish abbreviation) establishes that the State has priority over private actors in generation and commercialization activities and adopts binding planning (known in spanish as planeación vinculante) as the mechanism the Energy Secretariat (SENER) must use to enforce this preference.

According to the law’s regulations, prevalence is calculated annually in February, when SENER determines the total energy injected into the grid and the energy injected by CFE through its own plants or those considered State-participation projects, such as:

- Long-term producers. Equivalent to Independent Power Producers but required to sell all electricity exclusively to CFE. At the end of the contract, CFE may request to acquire the plant. Since all energy is sold to the State, this fully counts toward State prevalence. Investment is entirely private.

- Mixed projects. State participation occurs through trusts or development banks, not necessarily through CFE. According to the regulation of Electric Industry Law, the State must hold 54% of the equity, which may not need to be in cash. These plants can sell energy to both CFE and the wholesale market, counting toward both the 54% State quota and the 46% private quota.

- Other projects that SENER may designate as needed.

In addition to the annual calculation, SENER also estimates prevalence prospectively, based on estimation of supply and demand from the Secretariat. If the State’s 54% share is not met, strategic State projects are prioritized for permits and approvals to maintain prevalence. Regarding electricity commercialization, neither the law nor the regulations clarify how prevalence is calculated.

2.1 Binding Planning as a Mechanism to Ensure State Prevalence

Under the new rules, the sector authority is obligated to ensure that State prevalence is respected. This requires controlling the permits granted to private investors and closely monitoring the progress of projects assigned to the State, in any form of private participation.

This represents a significant shift from the 2013 model of free competition in electricity generation and commercialization. Understanding how the authority will implement it is therefore crucial. On October 16, 2025, SENER published in the Official Federal Gazette the Sectoral Electricity Plan (a planning document) along with two other documents that provide a clear and comprehensive picture of how this process will be executed.

The first document contains general administrative provisions, establishing the criteria that the National Energy Commission (CNE, by its Spanish abbreviation) must consider when approving or denying permits, in accordance with binding planning. These seven elements are:

- Contribution to meeting demand and electricity accessibility

- Reliability, continuity, quality, and safety of the National Electric System

- Efficiency in the Electric Sector

- Energy Transition and Sustainability of the National Electric System

- Prevalence

- Energy Justice

- Innovation and Technological Development

The second document issues a call for private investors interested in developing 100% private electricity generation plants to submit their applications to SENER, which will evaluate them based on the criteria outlined in the call.

Projects that qualify will be considered strategic by SENER and, therefore, will benefit from streamlined approval processes. However, under the current rules for private generation, the State determines all project elements, while private investors assume the costs.

For example, the State decides where each plant will be built, which renewable technology will be used (wind or photovoltaic, not natural gas), where it will interconnect to the National Electric System (which is the CFE substation for interconnection), and the project’s expected commercial operation date. All this involves highly constrained planning horizons, acceptance deadlines, and expensive connection studies. An example of this is that private investors must formally accept the costs of reinforcement and interconnection works defined by CENACE before permits are issued.

Notably, the largest pre-permit costs stem from connecting to transmission lines within the CFE-owned substation. This is not standard industry practice, as typically the substation owner assumes interconnection costs. In Mexico, CFE is responsible for the substations receiving new renewable energy generation projects.

Private investors, whether domestic or foreign, must accept the call on its terms, covering planning expenses and financial commitments before the permit is granted, and declare interest within a very short time frame—only five business days from the October 17, 2025 call.

This compressed planning horizon forces investors to make large upfront payments while having very little time to decide and inform the National Energy Commission of their participation interest, until the next call, whose date remains uncertain.

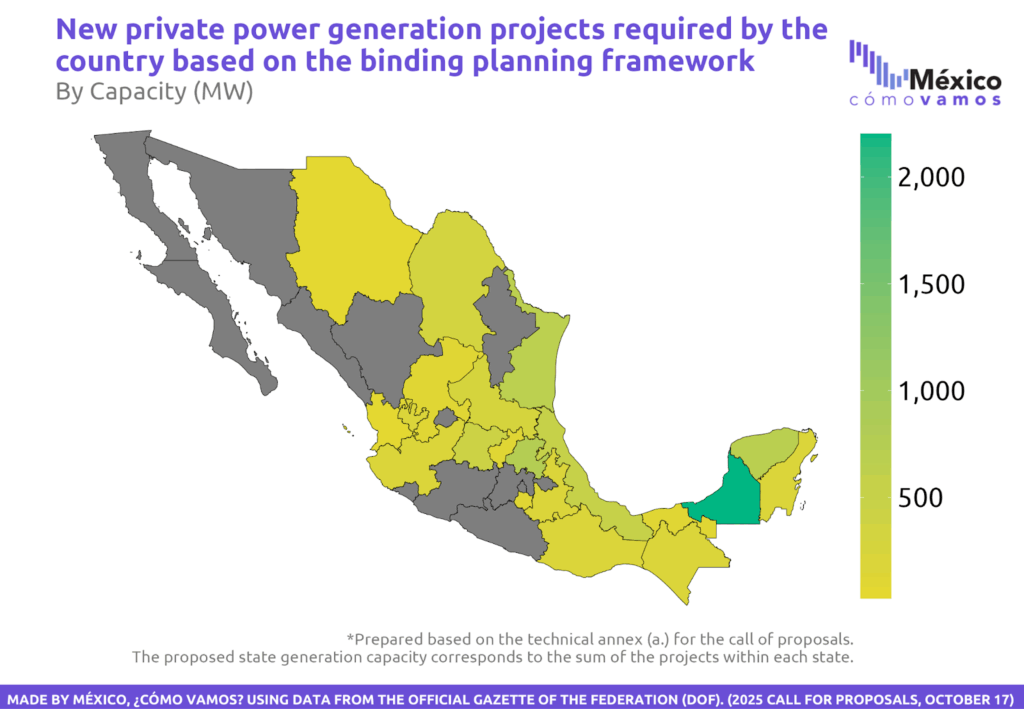

The call specifies, by electrical region, the required capacity (MW) and the generation technology mandated by the authority. For this instance, it includes renewable technologies, both photovoltaic and wind, specifies the interconnection substation, and calculates the investment amount the private party must make to reinforce the substation to expand capacity.

In short, SENER plans the required capacity and locations, issues the call, private investors respond, the CNE evaluates the applications, and permits are granted accordingly. However, transparency remains an open issue, as the criteria allow considerable discretion. If multiple applications meet the criteria, comparison is necessary to determine a winner, which is not straightforward since each project is unique. Additionally, publishing the interconnection substation location generates land speculation around the site, potentially raising project costs significantly.

Four recommendations to improve binding planning:

- Open the planning process, including the determination of the upcoming State and private projects, to multiple stakeholders (academic, business, civil society, and government) to define projects listed in the call.

- Establish realistic planning horizons for deciding and notifying the CNE of interest of participating in renewable projects, as well as fulfilling payments (e.g., interconnection studies).

- Create technical instruments (e.g., algorithms) to facilitate fair comparison of applications and enhance transparency.

- Accelerate transmission and substation reinforcement to avoid high interconnection costs imposed on private investors.

3. Expected Participation of the Private Sector

In electricity generation, the private sector can participate jointly with the State through the forms defined in the previous section, including long-term producers, mixed projects, or other arrangements. Additionally, private investors may develop generation plants that compete directly with CFE, provided these plants are included in the binding planning. In other words, the authority calculates the amount of energy that private parties can inject into the grid without exceeding their 46% constitutional share.

Self-consumption is another option, consisting of generation plants of up to 20 MW that private investors can build to supply a specific group of end-users, such as an industrial park. Any excess energy produced must be sold to CFE, although it remains unclear whether the price will be determined by the market or CFE itself. There is also a non-grid-connected version of self-consumption, which must include backup capacity.

According to the Draft General Administrative Provisions for Binding Planning published by SENER, both types of self-consumption are not subject to binding planning. This means that the permits for these facilities do not need to comply with the criteria outlined in these provisions and are not included in the official call.

Overall, private sector participation under the new model is broad, offering multiple pathways to engage with the State while still allowing competition in electricity generation within the 54/46 constitutional framework.

However, incentives are biased toward partnerships with the State, unless private projects are included in binding planning. This is due to factors such as:

- The prevalence of the State, which limits permits for private competition even when it might be more efficient than CFE.

- CFE, as an integrated monopoly, is exempt from competition regulation, while private participants are not.

- Electricity dispatch rules will be respected according to the law and regulation, but reliability criteria apply, meaning that State plants —including natural gas facilities and even CFE coal or diesel plants— are likely to operate under “must-run” status. This ensures system reliability regardless of economic merit.

The planning criteria may also apply to State participation projects, but only a priori; that is, the authority considers that these projects already meet the requirements and are entitled to permits and authorizations.

According to this plan, the administration’s goal is to add 28,004 MW of new capacity by the end of the six-year term. Of this total, 68% will come from renewable technologies, and if clean sources such as hydroelectric and bioenergy are included, clean energy will represent 80% of the additions.

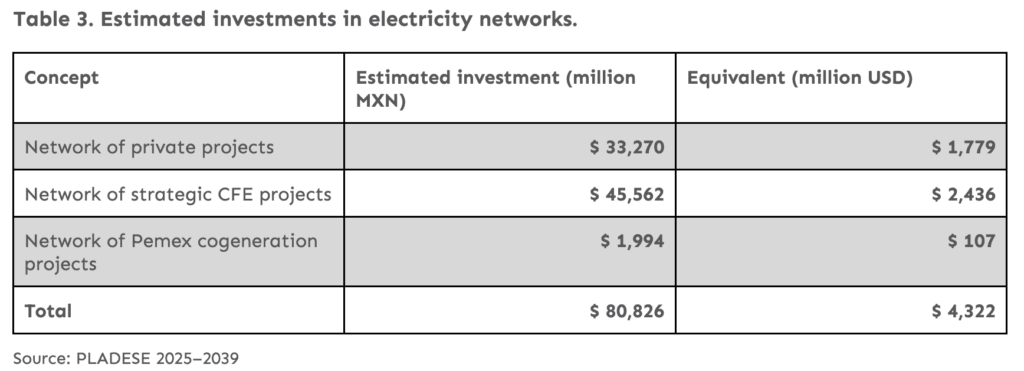

Expected investments in transmission and distributionAccording to the PLADESE, approximately $4.3 billion USD will be required during this administration to modernize and expand the transmission and distribution networks — investments that only CFE is legally authorized to make, not private entities. This figure is significantly lower than the amounts disclosed in earlier official presentations, highlighting inconsistencies in the estimation of generation, transmission, and distribution needs.

Financing of planned projects:

Under binding planning, most plants are public–private partnership projects regulated by energy laws. This means that most of the expected investment will come from private investors, and in only a few cases will the State need to make a contribution — which does not necessarily have to be in cash.

Public funding will be required only for the plants developed directly by CFE. It is estimated that the plants using fuel and already included in the PLADESE will fall under CFE’s responsibility, so public investment is expected to total around $5 billion USD.

Regarding transmission and distribution lines, CFE’s current law establishes a special subsidiary regime that gives the company broad flexibility to enter contracts and partnerships. Under this framework, CFE could find alternative financing mechanisms for transmission and distribution networks without relying on the federal budget (known in Spanish as PEF). It is worth noting that the Regulation of the Electric Sector Law (LESE) sets guidelines for private financing of transmission and distribution lines, which may contradict CFE’s own legal framework.The main challenge for the authorities will be designing contracts with private investors that align private interests with those of the State.

5. Analysis of Electricity Demand Integrated into Binding Planning

The PLADESE was developed based on an estimated annual growth rate of 2.5% for a 15-year period (2025–2039), consistent with the projected average GDP growth over the same timeframe. This expected behavior is grounded in several assumptions: reduced electricity losses, greater energy efficiency, increased participation of distributed generation, and a gradual incorporation of electric transport.

In other words, the economic growth embedded in these electricity projections may seem modest, but it reflects a realistic outlook given current trends in investment indicators in the country.

Regarding the composition of the electricity matrix, data from the first nine months of 2025 show that 65% of total power generation came from natural gas. It is worth highlighting the limited participation of hydroelectric generation (8% of the total)—even in a year of unusually heavy rainfall—and the fact that there is no guarantee this trend will continue in the future. In other words, hydroelectric generation cannot be assured at current levels, which has important implications for the configuration of Mexico’s future electricity mix.

According to PLADESE, the clean energy target (renewable + hydroelectric + nuclear) for 2030 is 38% of total generation, a figure that compares favorably with the 23% recorded between January and September 2025.

6. Transparency and Best Practices in the Energy Model

The CFE law subjects the Commission to the transparency, auditing, and accountability laws currently in force, under which it is clear that the Commission has lost autonomy from the executive branch.

Under the now-extinct 2013 legal framework, CFE Basic Supply was required to acquire its electricity hedges through transparent and competitive processes, namely electricity auctions. Under the current framework, these hedges will instead be acquired through state-developed power plants.

As a result, it is unclear whether the allocation of public-private partnership projects will be conducted through competitive and transparent processes, such as international auctions, or whether they will be handled via limited invitations or even direct allocations.

The extreme concentration of decision-making power in the context of binding planning is another aspect that warrants close attention.

7. Risks and Advantages of the New Model

The current energy model gives the State a preferential role in the electricity sector. It authorizes CFE to operate as an integrated monopoly and provides an exemption from the competition law. Recognizing the State’s inefficiencies, the model does not aim to reduce electricity tariffs, but rather to maintain them adjusted for inflation.

This asymmetry naturally incentivizes private investors to feel protected when partnering with the State. There is no doubt that private capital exists to develop the plants, and that there are companies interested in undertaking projects jointly with the State.

The challenges lie in the specific terms of each contract. Issues such as plant operation, dispute resolution, risk allocation, clarity in price definitions, force majeure, and others are crucial for encouraging investors to participate, both as State partners and as competitors in a market where, by constitutional definition, the State is the primary player. These risks are unique to the electricity sector, but systemic risks—such as challenges to judicial independence, changes to amparo law, and the review process under USMCA—also apply, with the terms only to be known in 2026.

There are also systemic advantages, all related to Mexico’s position as the United States’ main trading partner, highlighting the relevance of the USMCA review. The new model establishes rules that depart from the degree of openness in place when the USMCA was signed in November 2018, for the following reasons:

- The Constitution establishes prevalence in electricity generation and commercialization, but does not reference hydrocarbons. The legal framework was designed to also give Pemex a prevalent role, even without a predefined market share.

- Binding planning is a mechanism that limits private permits, which did not exist in 2018. Permits that appear clear for private actors are only those published in the specific call for projects mentioned in this document.

- With the signing of NAFTA (1993), natural gas no longer required an import permit. Under the new legal framework, this permit has been reinstated.

- Concentration of power in SENER by eliminating the independent regulator and replacing it with a legal, budgetary, and organizational unit dependent on the sector head.

Regardless of the effects on USMCA, binding planning aims to ensure that the State fulfills its role as supply guarantor, which limits private sector participation. By definition, private participation is conditional on the State generating 54% of electricity. Otherwise, the development and modernization of Mexico’s power system would be delayed, and the only existing mechanism is the additional allocation of State projects. Meaning that a delay could not be compensated by direct private investment due to the 54/46 requirement established by the Constitution.

For example, if private investors find the assigned geographic location unattractive, or deem the costs for transmission system upgrades too high, they may not build the project, delaying the necessary works.

8. Final Remarks

- State prevalence and reduced economic competition. The State’s prevalence in the electricity sector represents a significant departure from previous legal frameworks, where competition was more open.

- Binding planning gives the authorities a wide margin of discretion in granting permits to private actors.

- Private participation: limited by binding planning and constitutional production limits. Although private actors can participate in mixed projects, long-term producers, and self-consumption, as well as build plants that compete with CFE, their involvement is conditioned by binding planning and the constitutional 46% limit. Incentives favor partnerships with the State, and CFE operates as an integrated monopoly, exempt from competition regulation.

- Ambitious renewable energy goals, dependent on public-private co-investment. The 2025–2030 electricity plan aims to add 28,004 MW of capacity, with nearly 80% expected to come from clean or renewable energy. Total estimated investment in electricity generation will exceed $23 billion USD in public-private projects, in addition to significant investments in transmission and distribution.

- The success of PLADESE 2025–2039, particularly in the renewable energy component, will depend on reducing uncertainty for private investment, recognizing the constraints of limited fiscal space for increasing public investment in a context of fiscal consolidation and leveraging opportunities for collaboration with foreign trading partners, amid the USMCA review, the entry into force of the modernised EU-Mexico Global Agreement, and the need for long-term regulatory certainty.

- To receive priority consideration for generation and interconnection permits to the National Electric System, private investors must participate in the October 17, 2025 call and align with binding planning, which contains the technical and financial specifications for operating new renewable plants.

- The variety of private projects aligned with binding planning requires differentiated analysis depending on the project type (wind or photovoltaic), the socioeconomic characteristics of the project location and the required connection to the National Electric System (SEN).

- Limited transparency, incomplete rules, and lack of competition could hinder sector growth in the short and medium term. The new model prioritizes tariff stability over price reduction and poses transparency challenges, as the allocation of strategic projects may not be fully open or competitive, which could limit international best practices. Similarly, designating private projects as strategic—and therefore pre-approved—is subject to a high degree of discretion by the authorities.

- Systemic risks can threaten success, but solutions exist: efficiency, clarity and compliance. The success of the model depends on contract clarity, efficient plant operation and the State’s capacity to meet electricity supply commitments. Systemic risks relate to judicial independence and the USMCA review, which the new model imposes non-tariff barriers on, but there are also advantages stemming from Mexico’s trade relationship with the United States.

Sources:

Electricity Development Plan 2025-2030 (Available only in Spanish), published in the Official Federal Gazette of the Federation on October 17, 2025.

Priority call for generation permit applications (Available only in Spanish), Ministry of Energy.

México, ¿cómo vamos? (2025). Investment in Q2 2025 falls to 22.6% of GDP, the lowest level since Q3 2022. Available only in Spanish at: https://mexicocomovamos.mx/publicaciones/2025/09/inversion-en-el-2t2025-baja-a-22-6-del-pib-menor-nivel-desde-el-3t2022/